Problems with Probability

a quick look at prediction markets will show you how little the average person can comprehend it

I am a very active trader in prediction markets. And yes, I do believe the term trader is appropriate for what I do because I have a statistically significant track record of positive returns on all prediction market platforms that I trade on. Virtually every other user of prediction markets is a gambler—whether they understand it or not.

Take a quick look at the #crypto channel in the Kalshi discord and you’ll very regularly see people there thinking that they’ve found the ‘secret sauce’ in the 15 minute up/down markets. Most recently, I’ve seen a lot of people convinced that strategies along the lines of buying when price above X and time to expiration below T is profitable; these are people that use their phone to place market orders so they cross the full spread and pay taker fees.

I think part of the reason why this strategy can seem appealing, is that it makes money on the modal outcome, despite it being ridiculously negative in terms of expected value. In expectancy, it takes a while to realize it doesn’t work! Let’s walk through a basic example of how badly myself and the other market makers for these contracts would need to be pricing these contracts for this to be a long-term winning strategy.

Let’s assume that the strategy is to buy when the price is 95 cents (the side is irrelevant) and there is exactly 2 minutes left to expiration. I’ve gone over in a previous post1, how under Black76 assumptions, one needs to use effective time to expiry to account for the TWAP close mechanism. For now, just take my word that the way to adjust for this is to remove two thirds of the TWAP period from actual time to expiry to adjust to effective time to expiry. There’s a one minute TWAP, so we really have 80 seconds of effective time to expiry in the aforementioned setup. Let’s also just not account for interest rates (Kalshi pays interest based on the value of cash and positions in your account and there’s no margin, etcetera so the cost to tie up your capital isn’t really important from a risk neutral pricing perspective and it also will not meaningfully change the valuation at all anyway).

to convert from price to implied vol, we have:

T is fraction of a year and with 80 seconds we have:

Fees in the Kalshi crypto markets are:

Let’s compare the mid market of 94.5 cents (assume the market is 0.94@0.95 when these gamblers come in for their strategy) to their effective purchase price after fees of:

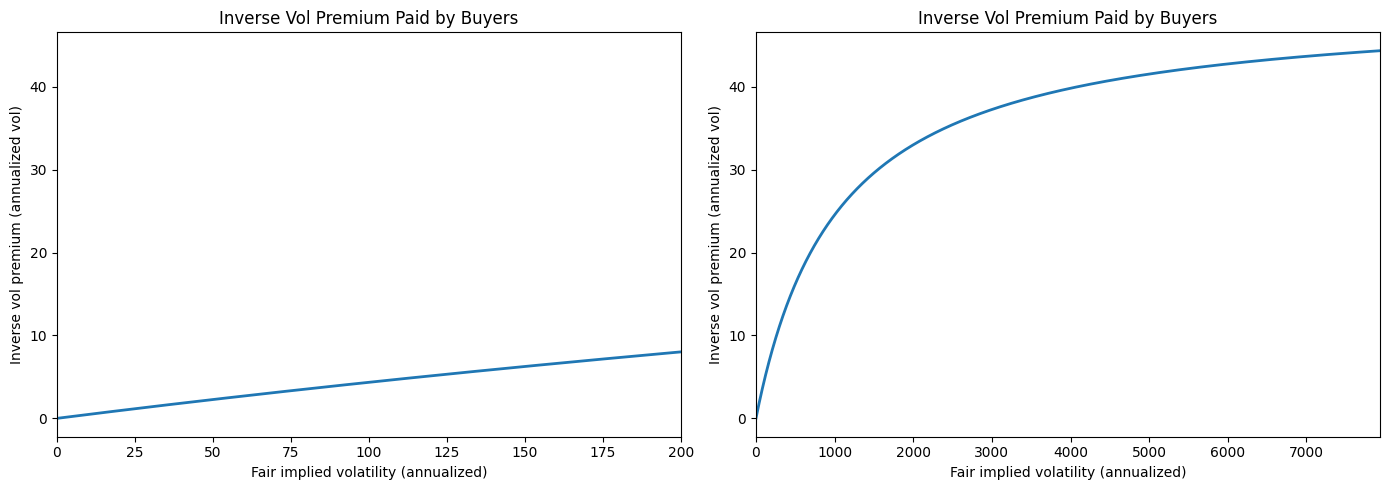

Now let’s plot out the implied volatility difference of mid market to the effective purchase price of these gamblers as a function of implied volatility:

When you buy a binary contract that is “in the money” you are effectively short vol, so the buyers of these contracts are selling vol for the amount shown in the graph below the implied vol of the mid-price. Admittedly, I had a hard time coming up with appropriate labels for the graph to adequately match what I’m trying to show, but hopefully it’s clear (enough)!

Hopefully it’s clear that that this premium changes as a function of implied vols of mid on the x-axis as different vols make it be viable to be 94.5 cents depending on the log moneyness of the contract with two minutes left. I included the graph on the right with unrealistically high vols to illustrate the concavity of this “premium”, because it looked too close to linear for more realistic vol numbers.

Anyway, the takeaway is that these gamblers are selling vol for 5-10 vol points below mid market! I mean what the fuck. Vol has to be so horrifically systematically overpriced for this to have positive expectancy it’s absurd.

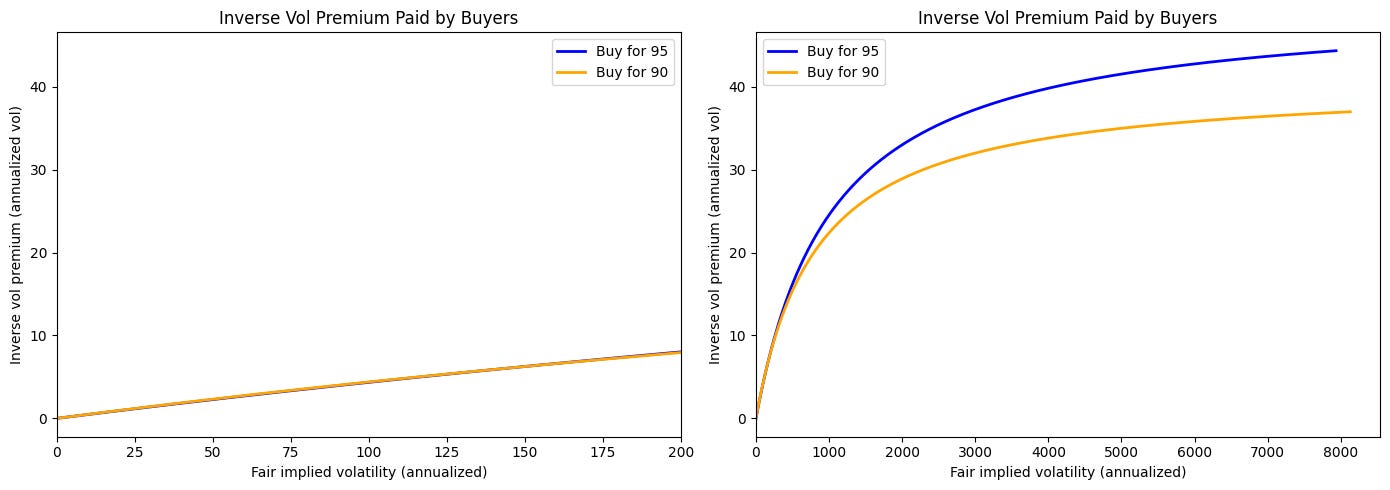

Just for shits and giggles, let’s do this plot for when the strategy is to buy when the price is 90 cents (mid is 89.5 cents) to show how the change in vol looks with different price thresholds. Any seasoned options trader should know which way the graph goes, but maybe it’s not obvious by the exact amount that it changes by.

The EV is worse despite the vol difference being less for the buy for 90 strategy though given that fees are directly proportional to variance and a Bernoulli with p=0.9 has higher variance than p=0.95.

These people also typically have some sort of stop loss logic; Kalshi doesn’t offer stop loss orders (yet). They will puke out of the position if the price gets below some X below their entry point so on trades where it at least (temporarily) does not go in their favor, they cross a second spread and pay fees a second time, but this time the fees are higher because a price closer to 0.5 will have a higher fee. Furthermore, a lot of the times the spread they cross will be even wider as they get closer to expiration as pricing the TWAP is a non trivial thing to do even with good spot and vol models as it now becomes path dependent.

It gets to be pretty hard to model out the actual total negative expectancy of this (even under assumptions of mid being fair) because of various puke out condition dynamics, but hopefully it’s pretty obvious that some strategy that relies on persistent and systematic overpricing of vol by multiple vol points without any sort of testing or own internal fairs of vols is moronic.